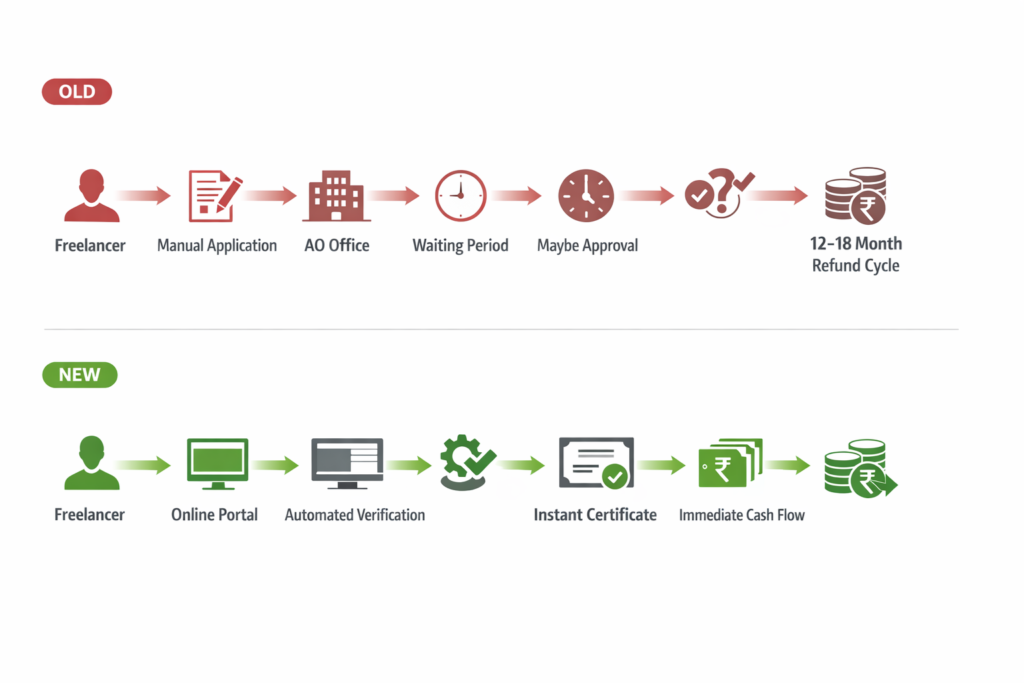

Before analyzing the specific legislative amendments, the following table visualizes the transition from the legacy manual system to the modern, automated framework introduced in this Budget.

| Feature | The Old Way (Pre-Budget 2026) | The New Reality (Budget 2026-27) |

|---|---|---|

| Lower/Nil TDS Certificate | Money is blocked for 12–18 months until the tax refund is processed. | Rule-Based Automated Process; instant issuance via online verification. |

| TDS Cash Flow | Foreign Asset Disclosure Window: 6-month amnesty for small taxpayers. | Instant Liquidity; tax not deducted if final liability is projected at zero. |

| Foreign Asset Disclosure | Risk of harsh penalties under Black Money Act for minor omissions. | Manual application to the Assessing Officer is prone to delays and discretion. |

| TCS on Foreign Tours | Tiered rates of 5% and 20% depending on transaction size. | TCS Reduction to 2%; a flat rate with no minimum threshold. |

| Revised Return Filing | Deadline of Dec 31; limited window for late corrections. | Manual application to the Assessing Officer; prone to delays and discretion. |

The “Silent Upgrade”

The Union Budget 2026-27 has followed a familiar cycle of public reception: initial disappointment over static income tax slabs followed by a slow, profound realization that the “Fine Print” contains game-changing administrative relief. For freelancers, small service providers, and middle-class investors, this is a “Silent Upgrade.” While headlines focus on the “No Change” reality of tax rates, the government has quietly engineered a structural overhaul of the compliance ecosystem.

The primary goal of these reforms is to fix the most persistent headache for the modern gig economy: chronic cash flow blockage. By shifting from an officer-led discretionary approval system to a rule-based automated framework, the administration is effectively ending the “interest-free loan” that millions of taxpayers were forced to provide to the state every year. For the “Global Indian” with small foreign assets, the Budget replaces legal anxiety with a pragmatic amnesty safety net. This analysis unpacks how Budget 2026 prioritizes liquidity and convenience over the political optics of rate cuts.

The “Rumor vs. Reality” Check

To address the immediate concerns of the salaried class, it must be explicitly stated that Income Tax Slabs remain unchanged for FY 2026-27. The New Tax Regime continues to be the default path, with the zero-tax threshold held steady to allow the significant reforms of previous years to fully take root. The government has prioritized a period of stability and certainty, choosing to focus its legislative energy on reforming the “Tax Year” framework and the administrative machinery rather than adjusting rates.

The Freelancer’s Victory: Automated Nil-Deduction Certificate

The centerpiece of the “Hidden Benefits” is the Rule-Based Automated Process for obtaining Nil Deduction Certificates. Historically, professionals and consultants were trapped by a rigid TDS system. Under Section 194J, a consultant might see 10% tax deducted from every invoice, even if their total annual income fell below the taxable limit. This resulted in significant liquidity being “locked” with the tax department for over a year until a refund could be processed.

Under the old rules, avoiding this required a manual application to a jurisdictional Assessing Officer (AO). This process was notoriously cumbersome, requiring physical documentation and often suffering from officer discretion or procedural delays. For a small freelancer, the time and cost involved often outweighed the potential liquidity benefit.

Budget 2026 removes this barrier entirely. Taxpayers can now apply for lower or nil deduction certificates through an online, rule-based system. The Income Tax Department will use a computerized mechanism to verify past records and income projections electronically. If predefined criteria are met, the certificate is issued automatically without a human interface. This is “Instant Cash” for the gig economy. Coupled with the new central submission of Form 15G/15H via depositories—which automatically pushes declarations to all relevant companies—the burden of repetitive paperwork has essentially been vaporized.

The “Global Indian” Safety Net: FAST-DS

For the modern Indian professional, failure to disclose a small foreign asset—such as a dormant US savings account from a student stint or a few ESOP shares from a global employer—once meant risking the full force of the Black Money Act. Recognizing this as a disproportionate burden on “accidental defaulters,” the government has launched the Foreign Asset Disclosure Window (FAST-DS).

This one-time, 6-month amnesty allows small taxpayers to regularize their records with immunity from prosecution.

- Category A: For those with undisclosed income or assets up to ₹1 crore, regularization requires paying a 30% tax on market value plus a 30% additional tax in lieu of penalty.

- Category B: For those who paid taxes but missed reporting the asset (up to ₹5 crore value), a nominal fee of ₹1 lakh grants full immunity.

Furthermore, permanent relief is provided for micro-assets: non-immovable foreign assets with an aggregate value under ₹20 lakh are now immune from prosecution retrospectively from October 1, 2024. This effectively protects middle-class professionals from life-altering legal consequences for minor, non-willful disclosure errors.

The “Deadline” Shift and TCS Relief

Administrative ease is further bolstered by the extension of the Revised Return Deadline to March 31. Previously, errors discovered after December 31 were notoriously difficult to rectify. The new provision grants taxpayers three additional months of “breathing room” to fix mistakes for a nominal fee—₹1,000 for income up to ₹5 lakh and ₹5,000 for others.

This relief is paired with staggered filing deadlines to reduce portal congestion. While individuals continue to file by July 31, non-audit businesses and trusts now have until August 31.

Travelers also receive a major “Hidden Benefit” through the TCS Reduction to 2% on overseas tour packages and medical/education remittances. By removing the previous 5% and 20% tiered slabs and the ₹10 lakh threshold for tours, the government has significantly lowered the upfront “cash drag” on international vacations.

Conclusion

The verdict on Budget 2026-27 is that it prioritizes financial plumbing over political optics. By automating the Nil Deduction Certificate, slashing TCS on tours to a flat 2%, and providing a safe exit for foreign asset disclosures, the government is returning time and liquidity to the small taxpayer. While the tax slabs remain a steady constant, the reduction in compliance friction is a significant win for the middle class. The government didn’t change the rate, but they stopped taking your money unnecessarily through procedural delays.

READ OUR OTHER ARTICLES

- Know the Real Reason Behind Tarun Kumar’s Death Over a Holi Balloon

The Holi festival turned tragic in southwest Delhi this year. On Wednesday, March 4, 2026, the narrow lanes of a JJ Colony in Uttam Nagar became the center of a … Read more

The Holi festival turned tragic in southwest Delhi this year. On Wednesday, March 4, 2026, the narrow lanes of a JJ Colony in Uttam Nagar became the center of a … Read more - T20 World Cup Final 2026: India vs New Zealand

The cricket world is getting ready for its biggest event. On Sunday, March 8, 2026, the T20 World Cup 2026 final will take place. The stage is set for a … Read more

The cricket world is getting ready for its biggest event. On Sunday, March 8, 2026, the T20 World Cup 2026 final will take place. The stage is set for a … Read more - 1,000-Year-Old Kakatiya Vishnu Idol Found in Telangana

The quiet forests of the Jayashankar Bhupalpally district in Telangana recently gave up a secret they had been keeping for a thousand years. In March 2026, as the summer heat … Read more

The quiet forests of the Jayashankar Bhupalpally district in Telangana recently gave up a secret they had been keeping for a thousand years. In March 2026, as the summer heat … Read more - Kerala Set to Manufacture BrahMos Missile on 180-Acre

India’s plan to become self-reliant in defense took a major leap forward on March 2, 2026. On this day, the Kerala Cabinet made a historic decision to give 180 acres … Read more

India’s plan to become self-reliant in defense took a major leap forward on March 2, 2026. On this day, the Kerala Cabinet made a historic decision to give 180 acres … Read more - Why Aman Gupta Chose His Birthday to Reveal OFF/BEAT ?

On March 3, 2026, the Indian startup world saw a digital shift that was as much about legacy as it was about the future. Aman Gupta, the famous co-founder of … Read more

On March 3, 2026, the Indian startup world saw a digital shift that was as much about legacy as it was about the future. Aman Gupta, the famous co-founder of … Read more